Life Cykel Cost analysis

LCC (Life Cycle Cost), or life cycle cost, which is the Swedish term, addresses all costs an object carries with it throughout its lifetime. An LCC analysis provides an overall economic assessment of the life cycle cost. The analysis also takes into account that money has a time value and that payments have different value depending on when they occur.

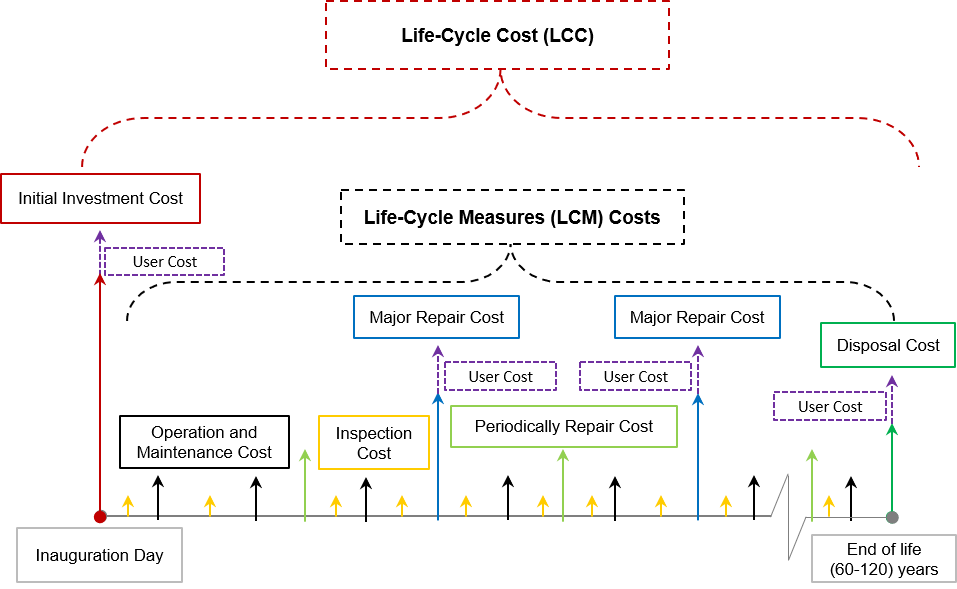

The LCC analysis thus takes into account not only the investment cost but also the costs required to keep the object sustainable for its lifetime. Inspection, operation, maintenance and repair, as well as demolition costs are included (Figure 1). Many times the current operating and maintenance costs have greater financial consequences than the investment expenditure. Consequently, the cheapest alternative from the investment cost point of view does not always mean the most cost-effective alternative in a life-cycle perspective.

Life cycle diagram and LCC categories

A life cycle diagram shows a schematic of an object’s life cycle and summarizes all the measures and costs needed to maintain the object’s function during its planned life cycle. The costs necessary to keep the item useful, and to give it full function, during its lifetime are called the cost of life cycle measures. Thus, the LCC of an object included in an LCC analysis includes both investment costs and costs for life cycle measures.

Objectives of LCC analysis

The goal of the LCC analysis is to minimize costs with regard to both investment costs and costs for life-cycle measures. Consequently, the most LCC-efficient item is not always the one that has the lowest cost of life-cycle measures or has the lowest investment cost or has the longest life. The most LCC-efficient item is the one that has the smallest total annual cost of investment, life cycle costs, and life expectancy.

Life span

By lifespan in LCC analysis, we mean economic lifespan that refers to the time period from the time the item is put into service until the cost of repair and maintenance measures (required to maintain the object’s intended function) becomes more expensive than replacing the item with a new one. To determine how long an object can maintain its intended function, we use the manufacturer’s specifications. Note that these apply provided that the manufacturer’s recommendations for use are complied with and that the object’s planned service and maintenance measures are implemented.

Methods for comparing costs

Money’s time value is central to LCC analysis as costs included in the analysis must be paid at different times. In order to compare costs paid at different times, these must be converted to a common time value. The most common method for comparing past, present and future costs with the present value is called the Net Present Value Method (NPV).

However, costs paid at different times need to take into account the discount rate to reflect the time value of payments. The present value is thus the calculated value of an investment’s future cash flow, discounted with respect to a given discount rate (calculation rate). Net Present Value is the difference between present value and investment cost.

The net present value method can be used both to decide whether a certain investment should be made or to compare different investment options. However, it is only possible to compare alternatives with the same economic life. If the life span is different, the annuity method is a better method.

The annuity method is closely linked to the present value method, but where the cost is stated per year, the effect of the investment’s lifetime. In LCC analysis, we use the annuity method to compare investment alternatives that have different lifetimes and can thus determine the most cost-effective alternative.

Applications of LLC analysis

Bridges

Demand for methodologists to analyze and evaluate alternative bridge designs has increased. The possibility of using LCC models (lifecycle cost models) for bridges has gained increasing interest in recent years, and the use of LCC analysis as one of several basis for decisions has now been accepted by several countries. The LCC analysis means that alternative bridge designs can already be estimated at an early stage on a lifetime basis. In this way, not only investment costs are taken into account, but also future costs, e.g. maintenance and repair costs.

Project Hjulstabron

The lake Mälaren has long been a hub and a facilitator for transport. Transport can be by sea, road or rail. The Swedish Transport Administration develops a roadmap for Hjulstabron to enable larger cargo vessels to traffic the fairway on Lake Mälaren. We have explored several alternatives, and now we have decided to move on with a low bridge, east of the existing one. But funding is still lacking.

LCC-analysis

In working with the roadmap, we have explored bridge alternatives, for example, to renovate the existing bridge or build a high bridge. We have also investigated several elevation options for a low bridge east of the existing Hjulstabron. We have chosen to proceed with a low bridge with a height of seven meters, to the east of the present Hjulstabron. The new bridge is proposed to have so-called double flaps, that is, there are two parts that open at the bridge opening.

Cost estimation, LCC analysis and climate calculation, as well as preparation of the basis calculation according to the successive method have been carried out.